1. Background

India is a major producer and exporter of cotton and its share in global production is 25 per cent (6132 million kgs of lint cotton in 2017-18). The area under cotton in 2017-18 was 11.3 million ha, which is 36 per cent of the global area under cotton. Cotton plays an important role in agrarian as well as industrial economy of the country. More than 7 million farmers derive their livelihood from cotton farming and in addition, more than 40 million people are involved in processing and trade of cotton. Cotton accounts for about 70 per cent of the basic raw material of the textile industries in the country. During 2015-16, the export of lint cotton was worth INR 11,400 crores.

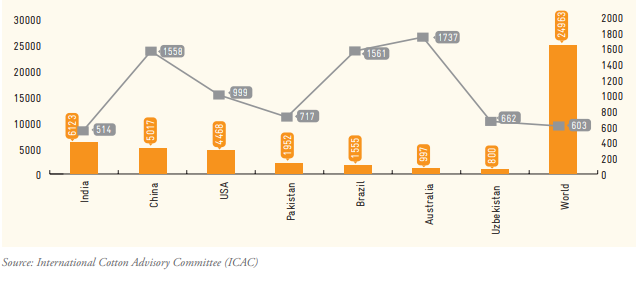

Across the globe, 70 countries are producing cotton and India tops the list among all the countries. However, altogether the yield of cotton is low among the top producing countries. While the yield of lint cotton is 1,737 kgs per ha in Australia; 1,561 kg/ha in Brazil and 1,558 kgs/ha in China, India produces only 541 kgs per ha.

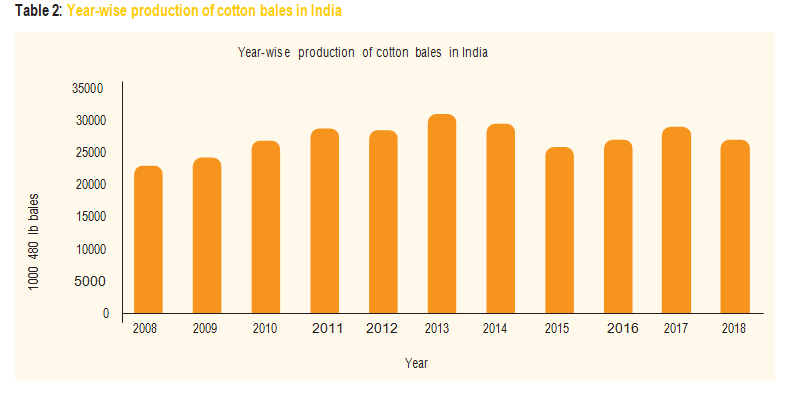

Table 2: Year-wise production of cotton bales in India

India produces about 95 per cent of Bt cotton leading to a demand in increased use of fertilisers and pesticides. From 50,000 ha in 2002, the area under Bt Cotton has increased to about 11 million ha.

Gujarat, Maharashtra, Telangana, Andhra Pradesh, Karnataka and Haryana comprise the top cotton producing states in the country with Karnataka and Haryana recording highest yields per ha.

Organic cotton

Organic cotton is grown using non-genetically modified plants (non-GMO) and without using any synthetic chemicals, fertilisers or pesticides. India, China and Turkey are currently into the production of organic cotton. However, the organic cotton market is in a nascent stage and comprises less than 0.47 per cent of the global cotton market (2014-15).

India is a global leader in the field of organic cotton. In 2015-16 the nation had a share of 56 per cent of the global production of organic cotton. There are 18 countries that produce certified organic cotton. According to the Textile Exchange Organic Cotton Market Report 2017, there were 192,148 organic cotton farmers in India. These organic cotton farmers produced 176,544 MT of cotton seed from 189,364 ha of certified organic area in 2015-16. In the same year, the in-conversion cotton area was 221,548 ha. However, the per ha yield of organic cotton fiber in India is around 500 kg per ha which compares unfavourably with countries like Turkey where the fiber yields are more than 1600 kg ha.

The increasing demand for organic cotton by the apparel brands worldwide provides enormous scope for organic cotton cultivation.

2. Challenges in Cultivation of Organic Cotton

2.1 Poor availability of non- GMO cotton seed

The major challenge faced by the organic farmers is the availability of quality non-GMO seeds. Most of the seeds available in the market are GMO seeds. Sometimes the available non-GMO seeds are already treated (may be contaminated). When non-GMO seeds are not readily available in the market, the farmers have to buy seeds of Bt Cotton.

2.2 Issues of GMO contamination

Maintaining traceability of the produce is a challenge with growing incidence of GMO contamination and chemical residues making their way into the certified organic products. The brands/processing industries reject the consignments sometimes as the contamination takes place at the post harvest stages. This is one of the reasons for the increase of in-conversion area in India as the auditors of organic certifying agencies have adopted very stringent standards for inspection and certification.

2.3 Lack of adequate extension services for organic farming

Despite growing attention on organic farming, there is a limitation on the promotional efforts. The support structure and services are also quite limited for farming as well as market access. Hence, the Government has adopted a dual approach. Both Bt Cotton as well as organic cotton are promoted by the Government. There is no restriction on the sale of GM seeds in the market, however, there is an inadequate effort by the Government to supply non-GMO seeds to the farmers.

2.4 No price premium for organic cotton

There is no special Minimum Selling Price (MSP)/ premium price for organic cotton fixed by the Government; hence farmers have little motivation and are not encouraged to adopt organic cotton farming.

2.5 Increased cost of certifications/compliances

The certification costs have gone up as many brands are asking for multiple certifications such as organic, Fairtrade, ethical practices etc. For export of cotton also various compliances need to be met if the product is going to the Europian Union (EU) or the United States of America (USA). There are also frequent changes in the compliances.

2.6 Price volatility and market assurance

Although with multiple certifications, the entire production may or may not be sold through organic and Fairtrade channels. The purchase price of seed cotton from the farmers is always linked to the international market price of cotton fibre.

2.7 Lack of adequate working capital

Cooperative and producer companies face challenges to access adequate working capital to procure the raw cotton from the farmers within a limited time. The holding capacity of the farmers is low and they want upfront payment of their produce or latest within a week’s time of procurement/sale.

The farmers require working capital for purchase of seeds, inputs and labour payments. Although some farmers may use their Kissan Credit Cards (KCCs) but a majority borrow from the private money lenders to meet their on-farm expenses.

2.8 Risk of weather variation

In the case of rainfed farming, weather variations affect the harvests; hence no guaranteed harvest from the farms. Often farmers get reduced harvest because of poor rain/long dry spell or heavy rain during the harvesting season.

3. Project Idea

Nearly 6 million small and marginal farmers are engaged in cotton cultivation in India which is the largest producer of cotton. But in recent times Bt Cotton farmers are facing a number of issues. Recurrent pest attacks, erratic rainfall, unsustainable water use and poor quality of seeds are making it difficult for the cotton farmers.

Organic cotton farming is an emerging narrative, that has the potential to bring sustainable and regenerative practices into cotton farming that have substantially lower input costs. Thus, making it a financially sustainable option for farmers. It is also ecologically and environmentally friendly due to the use of bio-fertilisers and bio-pesticides.

The project idea is to support individual farmers to cultivate organic cotton by providing them financial and technical support. It is also sought to assist the farmers in the marketing of organic cotton and enabling them to get premium prices for organic cotton.

The basic objective is to support FPOs of smallholders to promote the cultivation of organic cotton and also to establish a strong supply chain of organic and fairtrade cotton. The support can be envisaged at three levels as explained below:

- Support (grants/subsidies/credits) to farmers groups (Cooperatives/Self Help Groups (SHGs)/Joint Liability Groups (JLGs) of smallholders) for conversion from conventional/Bt Cotton to organic and fairtrade cotton.

- Support (grants/subsidies/credits) to FPOs (Cooperatives/Producer Companies etc. of smallholders) to strengthen the entire supply chain of organic and fairtrade cotton.

- Credit support to FPOs for procurement and trade of organic and fairtrade cotton.

3.1 Intervention strategies and convergence

For support to farmers groups

The support may be provided through a local competent NGO or an established FPO for the following interventions.

- Farmer mobilisation and sensitisation for the adoption of organic and fairtrade cotton farming.

- Training and extension services on a Package of Practices (POPs) for organic and fairtrade cotton farming.

- Compensation for certification cost (organic and fairtrade) maximum up to one ha of farmland.

- Credit/working capital for cultivation.

- Facilitate farmers to access good quality non-GMO seeds. PROJECT IDEA 03 6

- Facilitate farmers to go for crop insurance.

- Facilitate farmers to have linkages with Producer Organisations (POs) for the sale of organic and fairtrade cotton.

A cluster development approach will be adopted to have a minimum of 1500 acres (600 ha) of the area under organic and fairtrade cotton in a cluster. This will help minimising the overhead costs including administrative, monitoring, certification costs.

For support to FPOs to strengthen organic and fairtrade cotton supply chain:

- Support for farmer mobilisation and sensitisation for the adoption of organic and fairtrade cotton farming.

- Support for conducting training and extension services for the farmers on package of practices for organic and fairtrade cotton farming.

- Compensation for certification cost of farmers (organic and fairtrade) maximum up to one ha of farmland.

- Maintenance of a robust internal control system and system for traceability.

- Procurement of quality non-GMO seeds and supply to members.

- Provision of credit to the farmer members for cultivation costs-need based.

- Promote crop insurance and ensure farmers to go for crop insurance.

- Procurement of cotton from farmers.

- Ginning of cotton.

- Negotiate with different buyers for sale of organic and fairtrade cotton; annual price fixation etc.

- Agreements with the buyers and obtain pre-finance from the buyers.

- Convergence with various enabling schemes.

The funds can either flow directly to the FPO or through an NGO, which will have the overall responsibility of achieving the project objectives. Each project should have a minimum area of 600 ha under organic and fairtrade cotton.

For support to producer organisation for procurement and trade of organic and fairtrade cotton

A loan could be provided to FPOs for procurement and trade of cotton. The loan then will be utilised as working capital to purchase organic and fairtrade cotton from the member producers and for transportation, ginning, temporary storage as well as supplying lint cotton to the buyers.

3.2 Potential for upscaling

The demand for organic cotton is rising in the local as well as export markets. However, the availability of organic cotton is quite limited and perhaps this may be an appropriate time to promote cultivation and processing of organic cotton through an FPO.

This model has the potential to be replicated within Odisha as well as in states like Andhra Pradesh, Gujarat, Karnataka, Madhya Pradesh, Maharashtra and Tamil Nadu (with suitable modifications based on local requirements).

If required, exposure visits can be organised to Chetna Organics, Odisha for interested organisations to understand this model in detail.

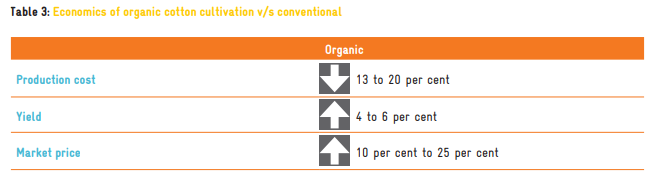

3.3 Comparison with conventional

Apart from a wide range of environmental benefits that emanate from the cultivation of organic cotton, from purely economic perspective studies have revealed lower cultivation costs and higher revenues for farmers engaged in organic cotton cultivation.

According to Eyhorn et. al. (2007)1 production costs of organic cotton were 13 per cent lower in 2003 and 20 per cent lower in 2004 than conventional cotton cultivation. The study revealed that the cost of seeds, fertilisers and manures, and pest management items were significantly lower in the case of organic cotton.

Productivity is another important factor that has an impact on the revenue of farmers. The above study also revealed that the productivity of organic cotton is 4 to 6 per cent higher than conventional cotton.

Market prices of organic cotton are also expected to be between 10 per cent to 25 per cent higher than that that of conventional cotton thereby resulting in an overall gain for the cultivators.

3.4 UPNRM case example

This project idea is based upon the model established by Chetna Organics, Odisha under the UPNRM. This model has been quite effective in promoting organic cultivation of cotton, enhancing incomes of farmers and also in establishing a strong supply chain of fair trade cotton through the establishment of a FPO.

The following are the highlights of this pilot:

- 4539 ha of land was brought under organic cultivation with the involvement of 2613 farmers across 4 clusters.

- Establishment of SHGs at the village level and an FPO across the 4 clusters.

- Farmers have improved capacities and POPs for organic cultivation.

- Time and effort saving technologies introduced by the FPO.

- Use of non-GMO seeds and organic pest control measures.

- Cost saving, productivity enhancement and higher revenues for farmers.

- Farmers able to grow intercrops with organic cotton that supplements their incomes.

- Marketing by FPO and better prices for farmers.

- Environment and biodiversity conservation owing to use of organic inputs/bio-agents and bio-fertilisers.

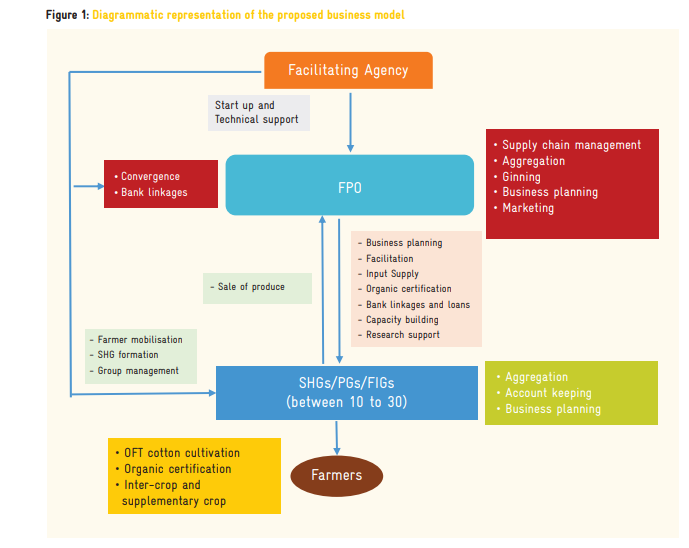

3.5 Business model with flow chart representation

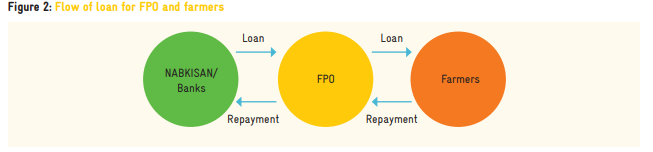

Under this model it is proposed that an established NGO can provide support in mobilisation of farmers into SHGs/ PGs/Farmer Interest Groups (FIGs) and later collectivise them in the form of an FPO.

The FPO could obtain loan (along with grant/subsidy, if applicable) from NABARD or commercial banks. The loan taken by the FPO would be for establishing a processing centre, establishment of systems for collection of produce from farmers, operational costs of processing centre as well as for meeting working capital requirements for purchase of farmer produce.

If required the FPO can also channelise loans for the farmers (through banks) after keeping a fixed margin on interest rates to meet its administrative cost.

The FPO is also required to build capacities of farmers in organic cultivation and also assist them in organic certification. For this purpose it could channelise funds from various government schemes, if possible, or utilise part of the loan funds.

The following flow chart represents the role of various institutions within the business model and also depicts the flow of inputs and outputs.

4. Impacts and Sustainability

4.1 Impacts- Social, Economic and Environmental

Social impacts

- Augmenting the availability of organic cotton seed that would be processed to produce edible oil and cattle feed devoid of chemicals, thereby preventing harmful chemical residues to enter human food chain.

- Inter-crops and other crops produced in organic fields are also free from chemical residues resulting in food safety and security.

- Collectivisation of farmers groups and strengthening the social infrastructure.

- Increased participation of women in livelihood activities.

- Building capacity of individual farmers and also farmer groups.

- The FPO generates additional employment for a number of persons.

Environmental impacts

- Reduction of soil, water and air pollution because of use of organic manures, FYM and organic pesticides and IPM.

- Organic soils retain more water.

- Increase in biodiversity, agri-biodiversity, micro-organisms etc.

- Eco-balance between pests and beneficial insecticides.

- Improved soil fertility.

4.2 Mainstreaming Options

This model has the potential to be replicated in various cotton growing belts within various parts of the country (with suitable modifications based on local requirements). To understand this model in detail exposure visits can be organised to Chetna Organics, Odisha for interested organisations.

4.3 Climate resilience or adaptability of the model

Climate change and climate variability manifesting in the form of low rainfall and higher temperatures are a major concern for cotton farmers. Climate resilience of any farm-based model is therefore critical for ensuring the success and sustainability of the model.

Several studies have shown that non-GMO seeds (used for organic cotton cultivation) are climate resilient. Such cotton varieties are expected to adapt more easily to changes such as extreme temperature and water fluctuations.

Moreover, the practice of organic farming is expected to enhance resilience in farming systems by ensuring better soil health and increasing organic soil matter which result in higher water retention in the soil.

4.4 Sustainability

Based on the experiences from Odisha and also the nature of the design of this model, it is strongly felt that after initial support for 2 to 3 years, this model would be able to achieve sustainability.

The major factors that are expected to contribute towards sustaining this model are:

- Facilitating agency to provide initial facilitation, startup and handholding support.

- Capacity building of SHGs/PGs/FIGs and FPOs in governance, business planning and financial management.

- Farmer groups to be linked with banks and bank loans provided to farmers.

- Convergence with ongoing government schemes to be achieved.

- The economics of this model indicate moderate to high returns from the farmers and the FPO.

- This model factors the cultivation of one crop only, however, farmers would be able to cultivate at least one more organic crop and hence this would result in even higher economic gains for the farmers.

- The economic analysis of FPO has been done based on processing of OFT cotton only. However, it is expected that the FPO would also engage in collection/processing of other organic farm produce and this would enhance its turnover and revenues.

5. Financial Details

5.1 Scope of financing and subsidy

At the FIG level, farmers would be requiring financial support in the form of loans for establishing NADEP compost pits. It is proposed that this requirement may be met partially through grant assistance from Paramparagat Krishi Vikas Yojana (PKVY) and partially from bank loans. In case culturable wastelands are to be brought under cultivation then funds from Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) may be utilised. The facilitating agency and/or the FPO would assist the farmers in convergence.

FPO may also facilitate the farmers to obtain loans for meeting their cultivation costs. These loans would be sourced from NABKISAN or other banks.

The FPO is expected to require capital assistance (for equipment) to the tune of INR 42 lakh and working capital assistance to the tune of INR 400 lakh (for 6 months each year). The working capital requirement would be primarily met through loans from NABARD and other banks while capital costs would be met partially through loans and partially through grant assistance from NABARD and from Ministry of Food Processing industries.

PKVY: Under PKVY farmers taking up organic farming (minimum group size of 50 farmers) are provided grant assistance of INR 20000 per acre spread over a three-year period. Farmers could utilise these funds for purchasing seed, crop harvesting and transportation of produce.

Small Farmers’ Agribusiness Consortium (SFAC) Scheme: SFAC supports the FPOs by extending the loan guarantee and equity capital support schemes: The following two schemes of SFAC would be helpful for the FPOs to leverage the loan from banks:

- Loan/ equity guarantee cover scheme: Loans to POs/FPOs/ FPCs under credit guarantee cover. Under this scheme FPOs can get term loan, working capital loan and or both. However, to be eligible to get the loan, the FPO must be 1 to 2 years old having audited balance sheet for at least one year and a minimum share capital of INR 3 lakh. The rate of interest is charged as per the NABARD refinancing rate. The loan is given up to 6 times of the net worth of FPOs or INR 1 Cr whichever is less.

- Equity Grant Fund Support to FPCs: The Equity Grant Fund (EGF) enables eligible FPCs to receive a grant equivalent in amount to the equity contribution of their shareholder in the FPC, thus enhancing the overall capital base of the FPC. The Scheme shall address nascent and emerging FPCs, which have paid up capital not exceeding INR 30 lakh as on the date of application.

NABKISAN’s support to newly formed FPOs: There is provision for the loans to emerging/nascent POs which are not in a position to provide collaterals. However, funding to such FPOs up to INR 50 lakh in the form of loan which depend purely on the merits and prospects of their business plan.

MGNREGA: In case unculturable wastelands, erstwhile fallow lands are proposed to be used for spice cultivation then under ‘land development works’ component of MGNREGA labour cost for bunding and land levelling are provided under this scheme.

5.2 Cost economics

The proposed business model provides estimates of cost-benefits at two levels i.e. at the level of individual farmer and at the level of the FPO for OFT cotton cultivation, processing and marketing.

5.2.1 Cost-benefit for farmers

The following table provides details of the expected cost of cultivation and the expected net revenue for individual farmers engaged in OFT cotton cultivation on one-acre land.

Table 4: Cost-benefits for individual farmers engaged in OFT cotton cultivation (1 acre landholding)

|

S.No |

Particulars |

Unit |

Organic Cultivation |

|

Total Cost (INR) |

|

|||

|

|

|

|

Quantity |

Cost (INR) |

Year 1 |

Year 2 |

Year 3 |

Year 4 |

Year 5 |

|

A.1 |

Capital Cost |

|

|

|

|

|

|

|

|

|

1.1 |

Compost pit - nadep (size - 3 m x 1.8 m and height 0.9 m and 23 cm thick wall) |

No |

1 |

14000 |

14000 |

0 |

0 |

0 |

0 |

|

|

Total A.1 |

|

|

|

14000 |

0 |

0 |

0 |

0 |

|

A.2 |

Recurring cost |

|

|

|

|

|

|

|

|

|

A.2.1 |

Land preparation and sowing |

|

|

|

|

|

|

|

|

|

1 |

Land preparation |

L/s |

|

|

2000 |

2100 |

2205 |

2315 |

2431 |

|

2 |

Seed |

Kg |

0.75 |

500 |

375 |

394 |

413 |

434 |

456 |

|

3 |

Inter-crop seed cost |

Kg |

1 |

200 |

200 |

210 |

221 |

232 |

243 |

|

4 |

Seed sowing |

Person days |

4 |

250 |

1000 |

1050 |

1103 |

1158 |

1216 |

|

|

Total A.2.1 |

|

|

|

3575 |

3754 |

3941 |

4139 |

4345 |

|

A.2.2 |

Main Field cultivation |

|

|

|

|

|

|

|

|

|

5 |

Manuring |

Tonnes |

4 |

1000 |

4000 |

4200 |

4410 |

4631 |

4862 |

|

6 |

Inter-cultivation practices |

Person days |

6 |

250 |

1500 |

1575 |

1654 |

1736 |

1823 |

|

S.No |

Particulars |

Unit |

Organic Cultivation |

|

Total Cost (INR) |

|

|||

|

|

|

|

Quantity |

Cost (INR) |

Year 1 |

Year 2 |

Year 3 |

Year 4 |

Year 5 |

|

7 |

Weeding |

Person days |

8 |

250 |

2000 |

2100 |

2205 |

2315 |

2431 |

|

8 |

Spraying |

Person days |

4 |

250 |

1000 |

1050 |

1103 |

1158 |

1216 |

|

9 |

Harvesting cost (cotton) |

Person days |

20 |

250 |

5000 |

5250 |

5513 |

5788 |

6078 |

|

10 |

Harvesting cost for pulses |

Person days |

5 |

250 |

1250 |

1313 |

1378 |

1447 |

1519 |

|

|

Total A.2.2 |

|

|

|

14750 |

15488 |

16262 |

17075 |

17929 |

|

A.2.3 |

Post harvest expenses |

|

|

|

|

|

|

|

|

|

12 |

Drying and grading |

Person days |

4 |

250 |

1000 |

1050 |

1103 |

1158 |

1216 |

|

13 |

Packaging and transportation cost |

Qtl |

1000 |

9 |

9000 |

9450 |

9923 |

10419 |

10940 |

|

|

Total A.2.3 |

|

|

|

10000 |

10500 |

11025 |

11576 |

12155 |

|

A.2.4 |

Other expenses |

|

|

|

|

|

|

|

|

|

14 |

Crop insurance per acre |

Per annum |

1 |

1700 |

1700 |

1700 |

1700 |

1700 |

1700 |

|

|

Total A.2.4 |

|

|

|

1700 |

1700 |

1700 |

1700 |

1700 |

|

|

Cost of Cultivation (A2.1+A2.2+A2.3+A2.4) |

|

|

|

30025 |

31441 |

32928 |

34490 |

36129 |

|

|

Total cost - capital cost and recurring cost |

|

|

|

44025 |

31441 |

32928 |

34490 |

36129 |

|

B |

Yield per Acre |

|

|

|

|

|

|

|

|

|

15 |

Cotton |

Qtl |

8 |

5200 |

41600 |

43680 |

50450 |

52973 |

55622 |

|

16 |

Pulses |

Qtl |

1.5 |

5000 |

7500 |

7875 |

9096 |

9550 |

10028 |

|

|

Total (B) |

|

|

|

49100 |

51555 |

59546 |

62523 |

65649 |

|

C |

Net Returns (B-A) |

|

|

|

19075 |

20114 |

26618 |

28034 |

29520 |

Assumptions

- The cost of cultivation may be sourced from the ongoing schemes of the Government, primarily PKVY wherein a subsidy for an individual farmer is provided for upto 3 years.

- If required the FPO could arrange bank loan for the farmers for construction of NADEP pit and for meeting the cost of cultivation for one year.

- Inflation at the rate of 5 per cent per annum has been factored in while calculating all costs as well as revenues.

- From the third year onwards it is assumed that the farmers would be able to get organic certification and a 10 per cent premium in price has been taken.

- The above assumption does not factor in drip irrigation system. In case drip irrigation is factored in then the yields are expected to increase by about 10 per cent to 20 per cent.

- The labour costs are included while calculating the above costs but in case farmer engages in performing various agricultural operations then the cost of labour may be a saving for the farmer.

- This model is based on yield estimates from Odisha. In case of other regions the yield may show slight variations.

Economic analysis

Under the proposed model, farmers are able to get a return of around INR 1.21 lakh, annualised over 5 years. While the net annual returns are around INR 0.19 lakh (Year 1 without deducting capital costs) to INR 0.29 lakh (Year 5). The benefit cost ratio for an individual farmer is calculated to be 1.56.

Table 5: Economic analysis of organic chilli cultivation in one-acre landholding

|

Particulars |

Amount in INR |

|||||

|

Year 1 |

Year 2 |

Year 3 |

Year 4 |

Year 5 |

Total |

|

|

Capital cost |

14000 |

0 |

0 |

0 |

0 |

|

|

Recurring cost |

30025 |

31441 |

32928 |

34490 |

36129 |

|

|

Total cost |

44025 |

31441 |

32928 |

34490 |

36129 |

179014 |

|

Total benefits |

49100 |

51555 |

59546 |

62523 |

65649 |

288374 |

|

Net benefits |

5075 |

20114 |

26618 |

28034 |

29520 |

109360 |

|

|

|

|

|

|

|

|

|

Net present worth of cost @15 per cent |

121423 |

|

|

|

|

|

|

Net present worth of benefits @15 per cent |

189265 |

|

|

|

|

|

|

Benefit Cost Ratio |

1.56 |

|

|

|

|

|

5.2.2 Cost-benefit for FPOs

Details of cost-benefit of FPO engaged in processing and marketing of OFT cotton is provided in the following table:

Table 6: Cost-benefits for FPO engaged in processing and marketing of OFT cotton (1500 acres)

|

S.No |

Particulars |

Unit |

Organic Cultivation |

Year 1 |

Year 2 |

Year 3 |

Year 4 |

Year 5 |

|

|

|

|

|

Quantity |

Cost (Rs.) |

|

(INR In Lakh) |

|

||

|

A.1 |

Capital Cost |

|

|

|

|

|

|

|

|

|

1.1 |

Storage (transit storage) cum office |

Sq. ft. |

1500 |

700 |

10.50 |

0.00 |

0.00 |

0.00 |

0.00 |

|

1.2 |

Office equipment (weighing machines, chairs, table, shelf, desktop computer, printer etc.) |

Lumpsum |

1 |

150000 |

1.50 |

0.00 |

0.00 |

0.00 |

0.00 |

|

1.3 |

Purchase of vehicle for transportation |

Nos |

1 |

1500000 |

15.00 |

0.00 |

0.00 |

0.00 |

0.00 |

|

1.4 |

Machinery and equipment (including weighing scale, storage racks, ginning machine etc.) |

Lumpsum |

|

|

15.00 |

|

|

|

|

|

|

Total capital cost |

|

|

|

42.00 |

0.00 |

0.00 |

0.00 |

0.00 |

|

A.2 |

Recurring cost |

|

|

|

|

|

|

|

|

|

2.1 |

Mobilisation of farmers, training and technical guidance on organic farming for 3 years |

Acre |

1500 |

500 |

7.50 |

7.88 |

8.27 |

0.00 |

0.00 |

|

2.2 |

Capacity building of farmers in POPs, primary processing etc |

Acre |

1500 |

500 |

7.50 |

7.88 |

8.27 |

0.00 |

0.00 |

|

2.3 |

Certification cost (including overheads) |

Acre |

1500 |

500 |

7.50 |

7.88 |

8.27 |

8.68 |

9.12 |

|

2.4 |

Procurement of seed cotton from the farmers @ 8 quintals from one acre |

Quintals |

12000 |

5200 |

624.00 |

655.20 |

756.76 |

794.59 |

834.32 |

|

S.No |

Particulars |

Unit |

Organic Cultivation |

Year 1 |

Year 2 |

Year 3 |

Year 4 |

Year 5 |

|

|

|

|

|

Quantity |

Cost (Rs.) |

|

(INR In Lakh) |

|

||

|

2.5 |

Processing of seed cotton to lint cotton (ginning cost, packing, labelling, insurance, fee to market committee etc.) |

Quintals |

12000 |

400 |

48.00 |

50.40 |

52.92 |

55.57 |

58.34 |

|

2.6 |

Staff, administration, travel, coordination, marketing etc. |

Month |

12 |

120000 |

14.40 |

15.12 |

15.88 |

16.67 |

17.50 |

|

2.7 |

Interest on loan for working capital (12 per cent) |

Half yearly |

|

|

24.00 |

24.00 |

24.00 |

24.00 |

24.00 |

|

2.8 |

Interest on loan for capital cost (12 per cent) |

Per annum |

|

|

5.04 |

4.68 |

4.29 |

3.84 |

3.34 |

|

|

Total recurring cost |

|

|

|

737.94 |

768.35 |

878.65 |

903.35 |

946.63 |

|

|

Total cost - capital and recurring |

|

|

|

779.94 |

768.35 |

878.65 |

903.35 |

946.63 |

|

A.3 |

Income/ Benefits |

|

|

|

|

|

|

|

|

|

3.1 |

Sale of lint cotton |

Quintals |

4560 |

13000 |

592.80 |

622.44 |

753.15 |

790.81 |

830.35 |

|

3.2 |

Sale of cotton seeds |

Quintals |

7200 |

2000 |

144.00 |

151.20 |

182.95 |

192.10 |

201.70 |

|

3.3 |

Sale of scrap |

Quintals |

240 |

500 |

1.20 |

1.26 |

1.32 |

1.39 |

1.46 |

|

|

Total Income |

|

12000 |

|

738.00 |

774.90 |

937.43 |

984.30 |

1033.51 |

|

|

Gross returns |

|

|

|

0.06 |

6.55 |

58.78 |

80.95 |

86.88 |

Assumptions

In the above analysis the following assumptions have been made:

- The above analysis assumes that the FPO is promoting cultivation of OFT cotton with around 1000 farmers cultivating an aggregated area of 1500 acres.

- The cost of cultivation/conversion to organic will be sourced from different schemes of the Government including PKVY.

- The available subsidy from various sources has not been factored in this model which has been prepared on the basis of maximum cost in order to assess economic viability.

- The FPO would assist the farmers in obtaining organic certification.

- The storage infrastructure will be made of low-cost materials.

- Loan will be obtained for INR 4.00 crores during the first year as working capital for procurement of produce from the farmers. This amount for procurement will be taken on loan for about 6 months each harvesting season.

- A loan of INR 0.42 crores would be obtained for meeting the capital costs.

- An increment of 5 per cent each year for price escalation in the market value of cotton (selling price) as well as a premium of 15 per cent (after organic certification) has been factored in from the 3rd year.

- An increment of 5 per cent each year for price escalation and that of 10 per cent (for organic certification) in the purchase price of cotton from the farmers has been factored in from the 3rd year.

- An increase of 5 per cent each year in the cost of processing has been factored.

- An increase of 5 per cent each year in the administrative costs has been factored.

- The staff of FPO will coordinate the entire business operation including monitoring of conversion of conventional to organic farming.

ECONOMIC ANALYSIS

It is evident from the table below that under the proposed business model the FPO would incur nearly break even in the first year (excluding capital costs) and in the second year the FPO is expected to get a modest revenue of INR 6 lakh and from the 3rd year onwards FPO is projected to obtain a net return of about INR 60 to 90 lakh per annum. However, the instalment of loan has not been factored in the current analysis. The benefit cost ratio is calculated to be 1.03.

Table 7: Economic analysis of operations of FPO

|

Particulars |

|

|

Amount in INR Lakh |

|

|

|

|

Year 1 |

Year 2 |

Year 3 |

Year 4 |

Year 5 |

Total |

|

|

Capital cost |

42 |

0 |

0 |

0 |

0 |

|

|

Recurring cost |

737.94 |

768.35 |

879 |

903 |

947 |

|

|

Total cost |

779.94 |

768.35 |

879 |

903 |

947 |

4277 |

|

Total benefits |

738 |

774.90 |

937 |

984 |

1034 |

4468 |

|

Net benefits |

-41.94 |

6.55 |

59 |

81 |

87 |

191 |

|

|

|

|

|

|

|

|

|

Net present worth of cost @15 per cent |

2825 |

|

|

|

|

|

|

Net present worth of benefits @15 per cent |

2921 |

|

|

|

|

|

|

Benefit Cost Ratio |

1.03 |

|

|

|

|

|

LOANS

It is envisaged that for this business model the FPO would require a loan of INR 42 lakh for capital expenditure and in the first year of operation a loan of INR 400 lakh for meeting the working capital requirements for procurement of cotton from farmers. The working capital would be required for 6 months each year.

Table 8: Working capital loan for FPO

|

|

|

|

INR in Lakh |

|

|

|

Working Capital Loan |

Year 1 |

Year 2 |

Year 3 |

Year 4 |

Year 5 |

|

Yearly Working Capital Requirement |

400 |

400 |

400 |

400 |

400 |

|

Repayment |

400 |

400 |

400 |

400 |

400 |

|

Interest on net working capital Loan (Diminishing) @ 12 per cent per annum |

24 |

24 |

24 |

24 |

24 |

The repayment of loan of INR 42 lakh for capital expenditure would be initiated from second year onwards and it is expected to be repaid over a period of 10 years.

Table 9: Capital expenditure loan for FPO

|

INR in Lakh |

||||||||||

|

Capital expenditure loan |

Y 1 |

Y 2 |

Y 3 |

Y 4 |

Y 5 |

Y 6 |

Y 7 |

Y 8 |

Y 9 |

Y 10 |

|

Capital expenditure |

42.00 |

0.00 |

0.00 |

0.00 |

0.00 |

0.00 |

0.00 |

0.00 |

|

|

|

Repayment |

0.00 |

8 |

8 |

8 |

8 |

8 |

8 |

8 |

8 |

6.26 |

|

Interest on capital loan (Diminishing) @ 12 per cent per annum |

5.04 |

4.68 |

4.29 |

3.84 |

3.34 |

2.78 |

2.16 |

1.46 |

0.67 |

0 |

|

Total loan outstanding |

58.24 |

54.03 |

49.31 |

44.03 |

38.11 |

31.49 |

24.07 |

15.75 |

6.44 |

0 |

Chapters

Download the detailed resource material to help understand the better functioning and best practices for FPO.